Understanding Financial Statements: A university degree helps in understanding how financial statements work and provide a comprehensive financial picture.

Knowledge of Accounting Concepts: Preparing financial statements requires a working knowledge of accounting concepts like double-entry accounting, accrual basis accounting, and the accounting cycle.

I got a university degree to learn how financial statements work and how those numbers come together to give you a comprehensive financial picture.

After all, preparing financial statements requires a working knowledge of accounting concepts like double-entry accounting, accrual basis accounting, and the accounting cycle.

But there’s good news.

Rather than taking on years of study, you can read this 15-minute guide to preparing financial statements — aka the income statement, statement of changes in equity, balance sheet, and cash flow statement — instead.

Financial statements are the business world's equivalent of a medical check-up. They offer a comprehensive overview of an organization's financial condition, including details about its profitability, cash flow, and overall worth.

There are four types of financial statements, each with a unique purpose:

Each one of these documents gives stakeholders such as investors, creditors, employees — even competitors — valuable insights about where a business stands financially.

Already overwhelmed with the idea of preparing these statements? Consider using financial reporting software to centralize your data and automate most of the reporting process.

Financial statements provide easy-to-understand, standardized insights into your company’s financial performance, capital structure, and cash flow. Stakeholders need this information to:

When preparing financial statements, you have two options:

Expert Tip: This is why financial statements are prepared in a specific order.

You may see large companies prepare financial statements following GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards).

While there is a difference in the accounting standards between GAAP and IFRS, the purpose of each financial statement remains the same.

A trial balance is a summary of open accounts in your books. Here’s how to prepare a trial balance:

Recording transactions is the gateway through which all the information needed to prepare financial statements flows. Sales, purchases, returns — every transaction impacts your financial statements.

The old-school method was to record these transactions in a journal; however, using accounting software means you can just enter transaction details into the accounting system - the system takes care of the rest.

The next step is to post journal entries to sub-ledger accounts, which are accounts that record details and provide more context than the overarching general ledger. Sales transactions are posted to the sales ledger, credit sales are recorded in the accounts receivable ledger, and so on - you get the idea.

The sub-ledger accounts are then aggregated into five general ledger categories (income, expenses, assets, liabilities, and equity).

Join our Newsletter

Join North America’s most innovative collective of Tech CFOs.

You may need to post adjusting entries before you start closing your accounts. Adjusting entries are generally for unrecognized income or expenses for the period. Here’s an example to help you understand what I mean.

Suppose your company lent $20,000 to a friend’s company, ABC Corp., on December 1, 2023. According to the agreement, interest is due every 12 months and the rate is 4% per annum.

You prepared financial statements on December 31, 2023. In the process, you recorded the $20,000 loan as an asset for your company, but what about the $66.67 interest outstanding for December [($20,000 x 4%) / 12]?

The interest would be an adjusting entry:

| Account | Debit | Credit |

| ABC Corp. interest receivable A/C (current asset) | $66.67 | - |

| Interest income A/C (income) | - | $66.67 |

A trial balance helps check the arithmetic accuracy of accounts. Remember that the trial balance doesn’t find other types of errors such as amounts posted in the wrong account.

All debits have corresponding credits - of equal amounts - according to double-entry accounting. For this reason, a trial balance is built to check if the debits and credits are equal; if the total debit and credit amounts are different, you’ll need to check for arithmetic errors.

To create a trial balance, you just need to list the balances of all accounts in your books and sum up the debit and credit balances. Accounting software would do this for you automatically.

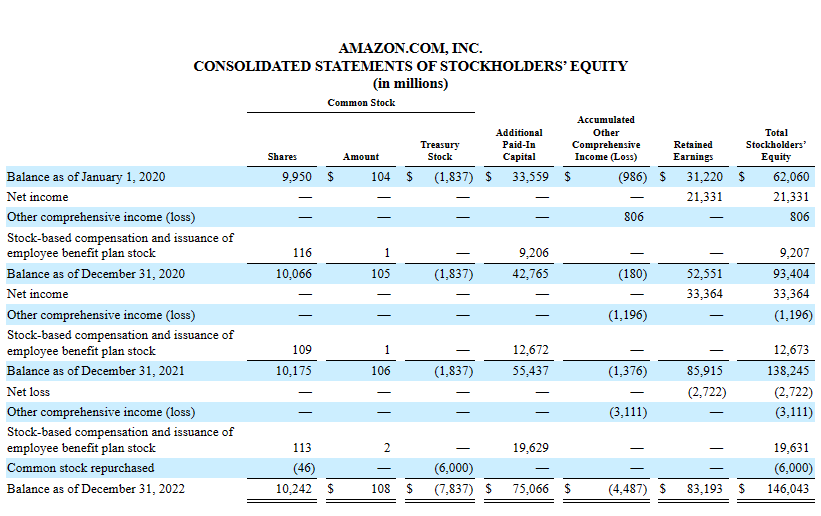

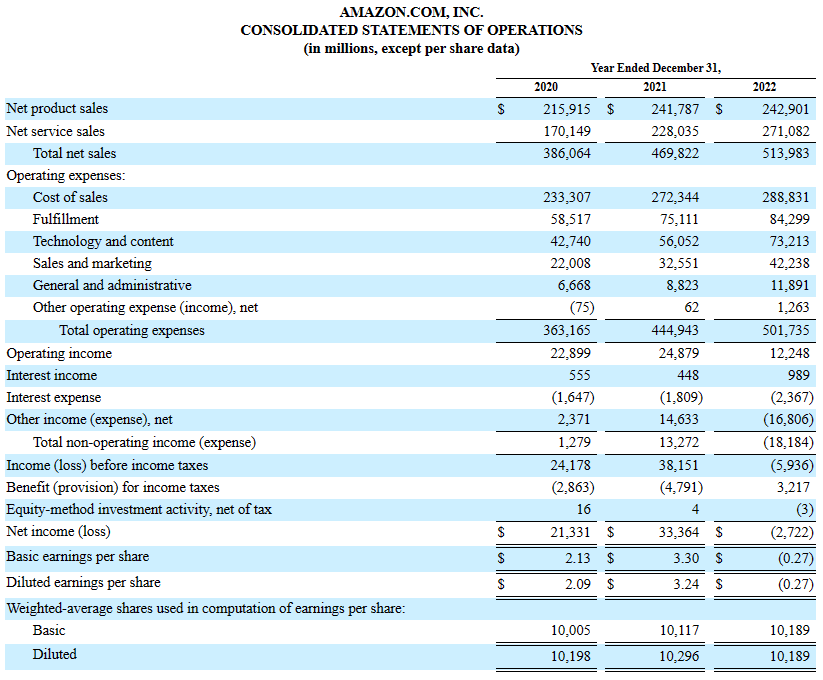

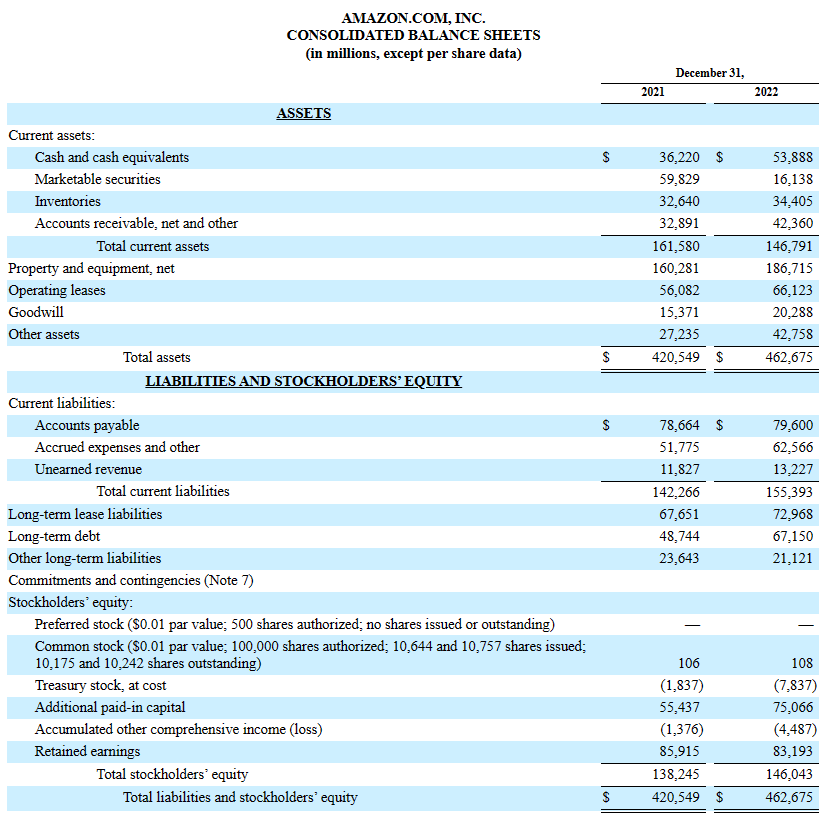

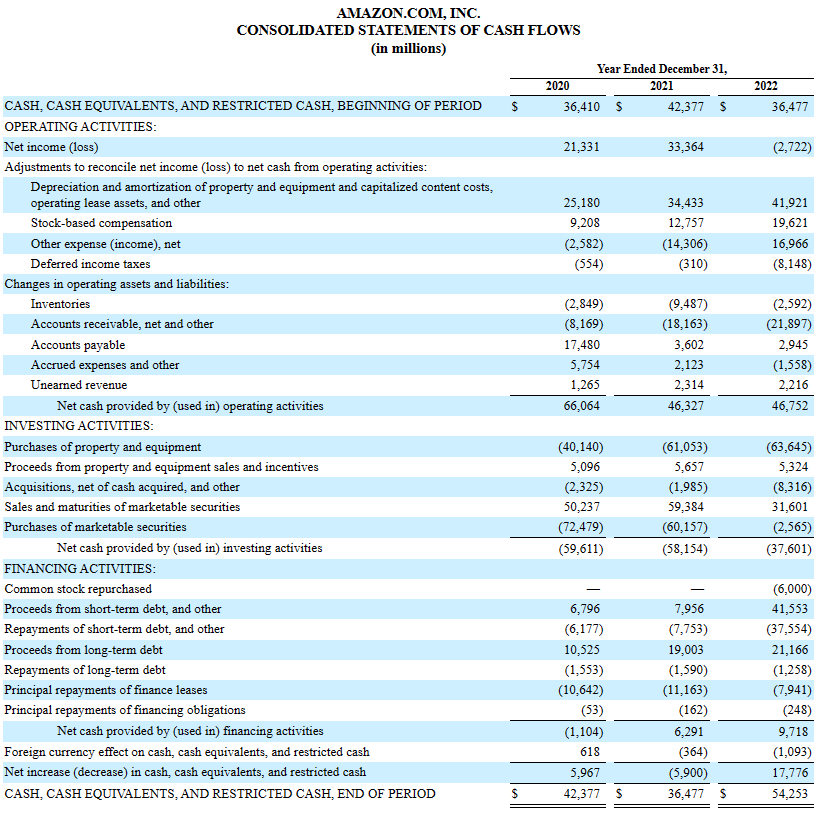

Let’s look at Amazon’s financial statements to help give context to each of these as I explain them, starting with the income statement.

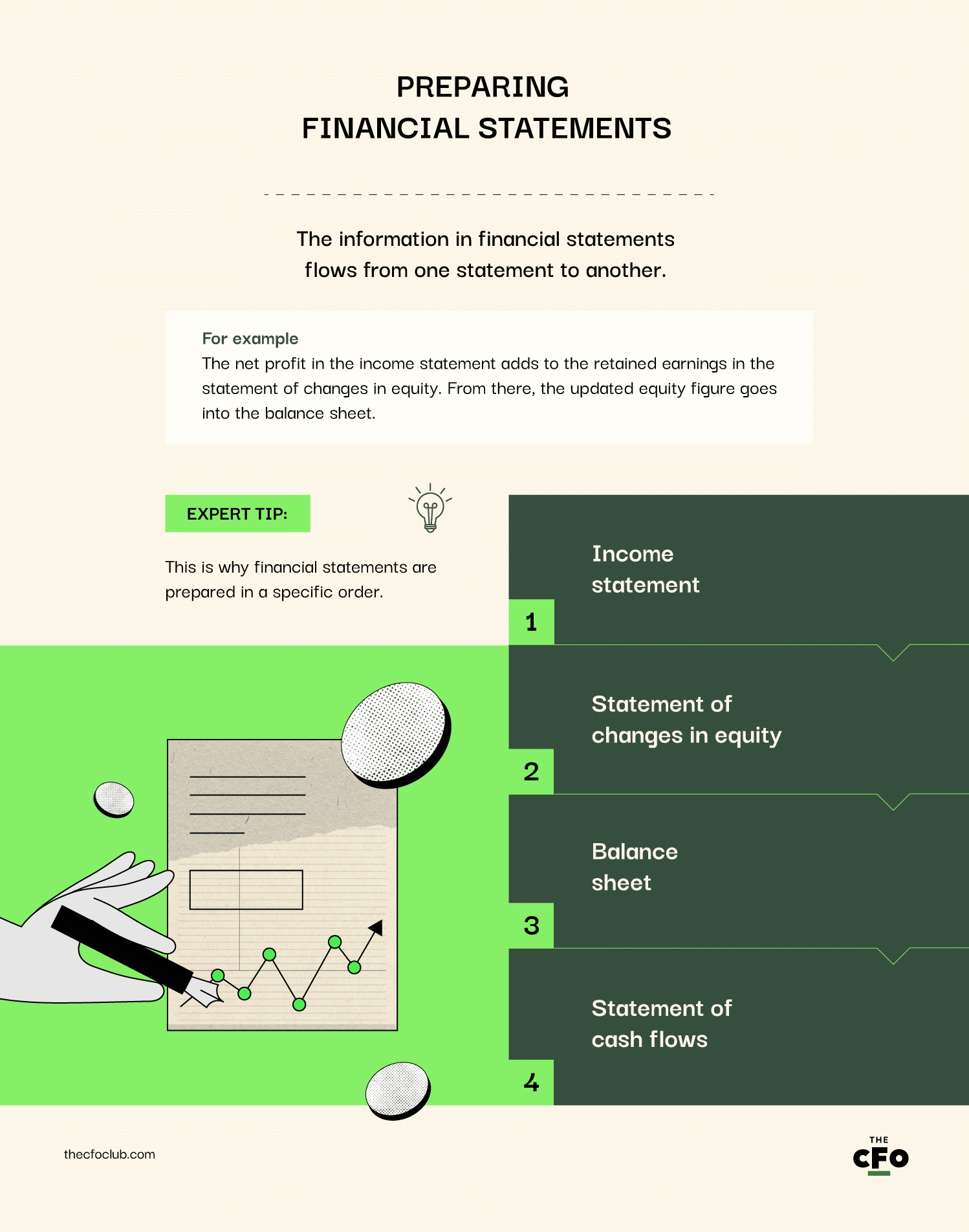

As I mentioned before, when preparing financial statements manually, you’ll want to start with the income statement. The sequence doesn’t matter when you use an accounting system.

The reason? The net income calculated at the end of the income statement is added to retained earnings, which is required to complete the statement of changes in equity. And the equity figure is needed to complete the balance sheet.

If you do this out of order, you’ll have a lot of repeated work.

Sum up all the sales during the period, net of returns. Don’t add any other types of income here, such as income from rent or interest — that’s not revenue.

Once you’ve added revenue to the top line:

Your SOCE starts with the opening balance in the shareholders’ equity (the total of common and preferred stock) from the beginning of the period (ie, what was on last year’s SOCE).

Then make the following adjustments in the SOCE:

Retained earnings are the portion of net income the company doesn’t distribute as dividends.

To calculate retained earnings:

Once you have the closing balance for the retained earnings account, add it to the opening balance of owners’ equity.

Other comprehensive income refers to gains and losses that don’t appear on the income statement because the company hasn’t realized them yet.

For example, if the company revalues an asset and it’s worth less, it’s the company's loss. However, the loss is only realized when the company sells that asset.

Items like foreign currency translation adjustments and changes in pension liabilities appear here.

If the company has issued new shares, add them here. If the company repurchases shares, subtract them from here.

Calculate the closing balance in stockholders’ equity and input this figure into the balance sheet.

I have good news.

You don’t have to compute most of the items in the balance sheet. This statement simply lists the balances of your accounts, which you would have calculated before preparing your trial balance.

Assets appear on the left side of the balance sheet. Balances of fixed asset accounts like land, current asset accounts like cash, and intangible asset accounts like goodwill appear here.

Liabilities are money the company owes. Balances of current liabilities like accounts payable and long-term liabilities like bonds appear here.

Shareholders’ equity is money that belongs to the company’s owners (equity shareholders) and preference shareholders.

Here’s a more intuitive way to look at it: Shareholders’ equity is the difference between assets (what the company owns) and liabilities (what the company owes).

The equity figure calculated when preparing the statement of changes in equity goes in this section.

Cash flow gives you insights into your business’s sources and uses of cash. Maintaining a healthy cash balance - aka, enough but not too much - is mission-critical.

For most startups, the problem is running out of cash. Monitoring the cash flow statement helps predict cash flow issues and prepare for them before they turn into a major problem.

The process of preparing a cash flow statement depends on whether you’re using the direct or indirect method.

However, both types of cash flow statements have three categories, which I’ll explain below. Summing up the cash inflows and outflows from these categories gives you the net cash inflow or outflow during the reporting period.

Cash flow from operating activities is the sum of cash inflow and outflow from activities like collection from debtors, payment to creditors, and taxes paid.

If you’re using the indirect method of preparing the cash flow statement, non-cash items like depreciation and amortization will also appear here.

Cash flow from investing activities includes cash received from the sale of securities and cash paid to buy new assets like land and equipment, among other things.

There are additional line items in this section as well if you’re using the indirect method. You’ll need to subtract gains and add back losses on the sale of assets.

This section includes activities like raising new capital, paying off debt, and paying dividends.

Using the indirect method? Subtract gains related to financing, like interest received, and add back financing expenses or losses, like interest paid.

Grasping all of this information can be overwhelming if you haven’t studied accounting, so here’s a recap:

You just need to understand what each financial statement tells you and where the information in those statements comes from. Accounting software takes care of all the mechanical tasks like preparing the trial balance, calculating the net income, and drawing the statement of cash flows.

Ready to compound your abilities as a finance leader? Subscribe to our newsletter for expert advice, guides, and recommendations from the finance leaders shaping the tech industry.

Arjun is an accountant-turned-writer. After a stint in equity research, he switched to writing for B2B brands full-time. Arjun has since written for investment firms, consultants, and SaaS brands in the Accounting and Finance space. He loves chatting about business, balance sheets, and burgers.

Follow the author: Opens new window TABLE OF CONTENTS